Have you ever tried to sort out life insurance on a packed weekday and thought, there’s no way I can squeeze in a medical exam? No exam life insurance makes that possible by giving you a fast, exam-free way to get covered without derailing your schedule.

In this guide, you’ll learn how these policies work, who qualifies, and what tradeoffs matter most. The goal is to help you understand your options quickly so you can choose coverage that fits your busy life without unnecessary stress.

How No-Exam Life Insurance Works

No exam life insurance skips the lab work and leans on digital records and health questions instead. Insurers look at things like prescriptions, driving history, and past diagnoses. The goal is faster approvals that don’t require you to meet with anyone.

Data-based underwriting can feel more streamlined. Your application moves more quickly, and you spend less time juggling schedules or trying to track old paperwork. For many adults, especially parents or professionals with limited flexibility, this approach feels far more realistic.

It also reduces the stress of waiting weeks for lab results or scheduling nurse visits that may not align with your availability. Many insurers now use automated tools that check multiple data sources at once, which cuts down on back-and-forth communication and helps you get a decision that feels transparent and easy to understand.

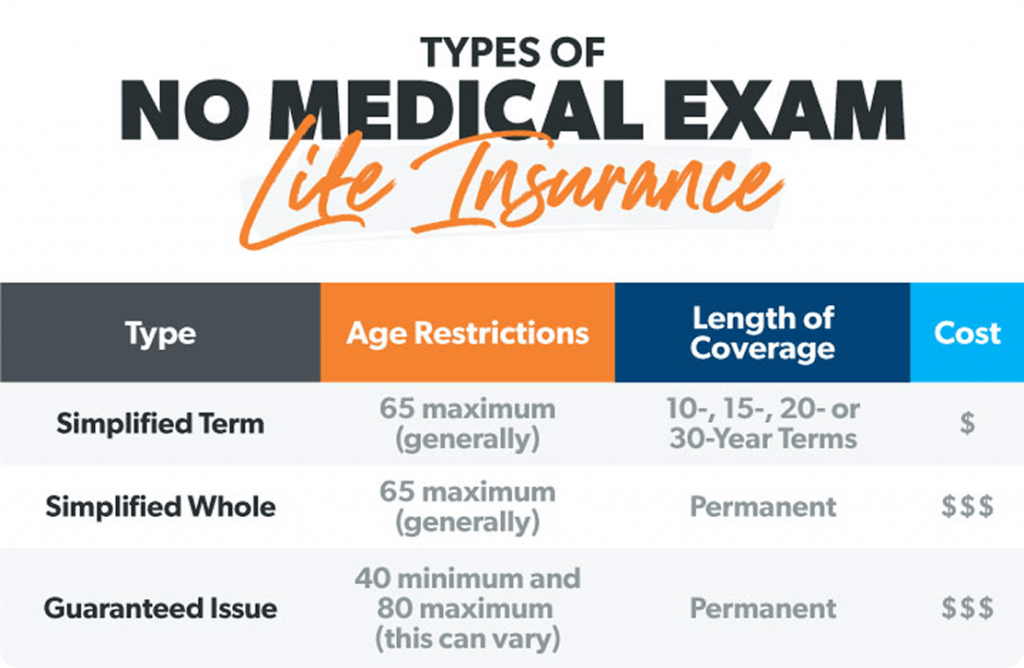

Types of No-Exam Coverage

No exam coverage comes in a few different forms, each designed for adults who want to avoid medical testing without sacrificing clarity or convenience. Understanding these categories makes it easier to choose the option that fits your health, schedule, and coverage goals.

source: wealthnation

Accelerated Underwriting

Accelerated underwriting uses automated checks to generate fast decisions. Healthy applicants with consistent records often qualify.

Some people get decisions within minutes. Coverage amounts tend to be higher than those of other no-exam options.

If your medical background is straightforward, accelerated underwriting can be the fastest route to meaningful coverage. It’s especially helpful if you don’t want delays caused by scheduling conflicts or missed appointments. More insurers have increased their coverage limits under these programs, which means you can often secure the protection you need without going through a traditional, time‑consuming process.

Simplified Issue

Simplified issue policies rely on a short set of health questions instead of full medical exams, which makes them appealing for anyone who wants a more direct path to coverage without extra appointments. They often suit adults with manageable health conditions or those who prefer a predictable approval experience.

When comparing options, looking at an overview of simplified issue life insurance can make it easier to understand how much convenience you prefer and what level of coverage aligns with your goals. These policies are also ideal if you’ve had minor health changes over the years that don’t fit neatly into automated systems but still want to skip the exam and move forward quickly.

Guaranteed Issue

Guaranteed issue coverage approves nearly everyone. It comes with the highest premiums and lower coverage limits.

A waiting period before full benefits activate is common. It’s often chosen by older adults or people with past declines.

Guaranteed issue isn’t usually the first stop, but it’s a safety net that helps when health barriers create friction elsewhere. It’s also a good option for people who simply want small, predictable coverage without answering medical questions.

A Quick Decision Checklist

Choosing between the different no-exam options can feel overwhelming when you’re short on time, so a simple guide can help you narrow things down quickly. Use these points to get a clearer sense of which type of policy matches your needs before you start an application.

- You want a fast, high coverage option

- You prefer predictable approval steps

- You need a fallback due to health concerns

These criteria help you sort between the three policy types in a matter of minutes.

Costs and Tradeoffs to Expect

No exam life insurance trades detailed testing for speed and convenience. When insurers take on more unknowns, they have to offset the risk. That often shows up in the form of higher premiums or capped coverage amounts.

Accelerated underwriting can still offer competitive pricing because the screening tools are more robust. The simplified issue often lands in the middle range.

Guaranteed issue is the most expensive per dollar of coverage because insurers accept the least information. It’s helpful to compare quotes from several insurers since pricing varies widely, and some companies specialize in fast-approval policies with more flexible guidelines.

Who Usually Qualifies for No-Exam Policies

Several factors determine which type of no-exam coverage you’ll be offered. Younger adults with clean medical histories are more likely to receive accelerated underwriting approvals. People with past or ongoing conditions often qualify for the simplified issue while still bypassing exams.

Guaranteed issue is open to nearly everyone regardless of health. Age ranges vary across insurers, but many offer it for older adults who need smaller policies to cover final expenses or supplemental needs. Even if you think your health might complicate things, there’s usually some form of no-exam policy available.

When to Gather More Records First

Some applicants can improve their results by briefly preparing before starting the process. If you’ve recently switched doctors or have inconsistent information in your digital health records, pulling everything together might help.

You may want to pause and gather details if any of these apply:

- You had major tests or procedures recently

- You changed prescriptions in the last month

- You suspect old records could delay processing

A little organization can make automated checks smoother and reduce follow-up requests later. It also helps ensure the insurer makes an accurate decision based on the most up-to-date information available.

Finding the Right Fit for Your Life

Choosing a no-exam policy ultimately comes down to how much time you have and how predictable you want the process to be. When speed and higher coverage matter, accelerated underwriting tends to win.

If you want simplicity without the exam risk, a simplified issue sits in a comfortable middle. Guaranteed issue is the path of last resort, but it gives access to coverage that might otherwise be out of reach.

Many adults find it helpful to compare these three paths side by side. Think about your goals, how urgently you need coverage, and how much information you’re comfortable providing. Matching the process to your lifestyle often leads to less stress and faster results.

Here’s a quick breakdown of what to prioritize before choosing a policy:

- How quickly do you need coverage to start

- How much medical history are you comfortable sharing

- Whether you prefer predictable pricing or maximum coverage

Your Next Step Toward Stress-Free Coverage

No exam life insurance has become a practical solution for adults balancing full schedules and family responsibilities. As you compare accelerated, simplified, and guaranteed options, focus on what matters most to you, whether that’s speed, cost, or predictability.

If you’d like more clarity before moving forward, exploring trusted resources from AccuQuote can help you feel more confident in your decision. Taking a few minutes now can make securing the right protection much easier and far less stressful.